Loading page...

Where should I put the money I save?

WHAT IS ASSET ALLOCATION?

You already know you need to save money. However, not all savings are created equal, and deciding where to put your savings is just as important as the percentage of your income you save.

This guide examines what the investing world calls asset allocation and why intelligent asset allocation models are the cornerstone of money management. Note that this is not to be considered investment advice. We recommend having a professional investment advisor create a tailored plan for your specific situation.

Unlock more top financial strategies at Business Mastery

LEARN MOREWHAT IS ASSET ALLOCATION?

Asset allocation means implementing a strategy that balances risk and reward by adjusting the percentage of your money you put into different “buckets” based on your risk tolerance, short- and long-term goals, and your time frame. Effective asset allocation strategies also consider enjoying your money while saving for the future so you can maintain a fulfilling lifestyle at every stage of life.

WHY IS ASSET ALLOCATION IMPORTANT?

Asset allocation allows you to diversify your investment portfolio, maximize your returns and minimize risk. Spreading your money among various investment classes means that volatility in any particular market won’t have an outsized effect on your overall portfolio. Over time, you’ll turn your savings into a reliable money-making machine that finances your future.

ASSET ALLOCATION MODELS

The “three-bucket model” is one of the most effective asset allocation models Tony teaches at “Unleash the Power Within.” It’s easy to use and understand and applies to any stage of life, whether you’re just starting in your career or on the home stretch to retirement.

THE THREE BUCKETS OF ASSET ALLOCATION

To divide your savings for maximum returns, consider asset allocation as three buckets: Your Security Bucket, your Risk/Growth Bucket, and your Dream Bucket. Wisely balancing these three areas allows you to grow your savings and move closer to financial independence. Put another way, think of these buckets as the backbone of your overall financial plan. While no two financial plans or asset allocation models will look the same, these objectives provide a structure that’s easy to reference and will help you visualize your end goal.

Minimize your risk by learning how to allocate your assets into these three buckets strategically. You can always add additional investment buckets to the list, but these three areas are the core of your financial future.

THE SECURITY BUCKET: STEADY AND SAFE

Your first bucket is the Security, or Peace of Mind, Bucket. This bucket gives you certainty in your life and acts as the cornerstone of your strategic asset allocation plan. It’s like the tortoise battling the hare – slow and steady wins the race. But here winning the race means not losing your life savings. If the Security Bucket were a car, it would be your family’s old Toyota or Volvo with 230,000 miles on it – not the flashy new Mercedes-Benz. The ride may not turn as many heads, but you know you’ll safely get to your destination.

Essentially, you keep the part of your nest egg you can’t afford to lose in your Security Bucket. It’s a sanctuary of safe investments that you lock up tight – and then hide the key. It’s one of the strategic asset allocation examples because it means you’re covered in case of an emergency.

So what kind of investments should you allocate to your Security Bucket? You want investment options with low volatility that you can rely on.

THESE INCLUDE:

- Cash/cash equivalents (such as money market funds with checking privileges)

- Bonds (such as TIPS, or Treasury Inflation-Protected Securities)

- Market-linked CDs

- Your home – An asset, but not an investment. This is your sacred sanctuary, so don’t “spend” it!

- Your pension (if you’re lucky enough to have one)

- Guaranteed annuities

- Your life insurance policy

- Structured notes (One with 100% principal protection, purchased through an Registered Investment Advisor)

These types of investments grow slowly, especially at first, but the power of compounding means asset allocation models that incorporate these investments may reap positive rewards in a secure environment over time. Experts would agree that this is step one, and the most crucial component of worthwhile asset allocation strategies. You can remember this Tony Robbins quote when you envision your Security Bucket: “Most everybody thinks that if I want to get big rewards I need to take huge risks, but if you keep thinking that, you’re going to be broke.”

THE RISK/GROWTH BUCKET: FAST AND VOLATILE

Money allocation focusing on the Risk/Growth Bucket are exciting because they can gain some truly amazing returns, but they are usually accompanied by volatility.

All effective business ventures inherently have some level of financial risk. That volatility shouldn’t scare you away, and the Risk/Growth Bucket isn’t just for serial risk-takers. It’s part of a well-rounded asset allocation strategy and often leads to the biggest returns in the end. Remember, the market will always rise and fall. The most successful investors know that you don’t get out when the going gets tough.

The bottom line? Whatever you put in your Risk/Growth Bucket, you have to be prepared to lose or live through volatility (depending on the risk of the investments). Take your time making this tough decision and choose wisely when deciding what percentage of your funds you want to place here.

What kind of investments fit into your Risk/Growth Bucket? These seven main asset classes fit the bill of potential high returns… or deep losses:

- Equities – Another word for stocks, or ownership shares of individual companies. Owning individual stocks is far riskier than vehicles for owning many of them at once, like mutual funds, index funds and exchange-traded funds (ETFs).

- High-yield bonds (aka junk bonds)

- Real estate

- Commodities (gold, silver, oil, coffee, cotton, etc.)

- Currencies

- Collectibles

- Structured notes (anything without 100% principal protection)

Depending on your personality type, it can be easy to get caught up in the idea of reaping great returns and forget how much you are risking in the process. It’s a balancing act, and proper asset allocation models involve finding the biggest rewards that come with the smallest amount of risk. That’s why proper diversification is key when deciding how to allocate savings. Ultimately, it’s the right mix of the Security and Risk/Growth Buckets makes for intelligent, strategic money allocation.

DON’T FORGET TO DIVERSIFY

Remember, don’t just diversify your savings between your buckets, but also diversify within them as well. As financial master Burton Malkiel shared with Tony, “Diversify across securities, across asset classes, across markets – and across time.” Spreading your money across different investments can decrease your risk and increase your upside returns over time.

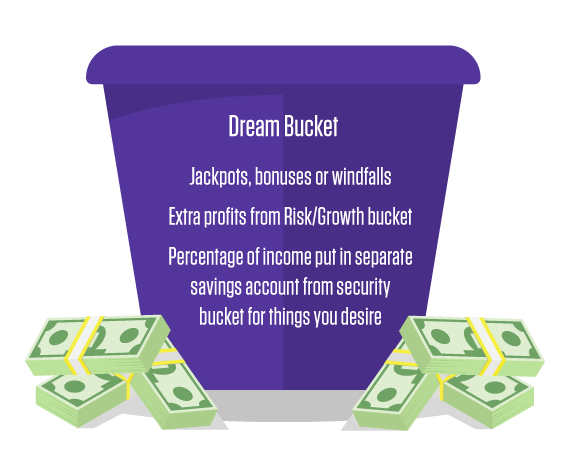

THE DREAM BUCKET: INVESTING IN FUN

The third and final bucket in this asset allocation strategy is for you to have fun with. With your Dream Bucket you set aside something for yourself and those you love so that all of you can enjoy life while you’re building your wealth. It’s meant to excite you, put some zest in your life so you want to earn and contribute even more. Sound silly? Think of the items you’re saving for in your Dream Bucket as strategic splurges. They’re a key part of sustainable asset allocation strategies, and also necessary for your own sense of fulfillment and peace of mind.

With this bucket, be creative. What can you not stop dreaming about? What would be a glorious experience you’ll remember forever? What would help you stay connected to your partner or reconnect with yourself? It could be season tickets to your favorite sports team or local theatre. Maybe a new car – one that isn’t so practical. Perhaps you fly a lot and dream of upgrading from Economy to Business Class? Your imagination is the limit. Remember that your dreams are not designed to give you a financial payoff; they are designed to give you a greater quality of life.

Don’t just save for the life you want. Make sure you live it by being realistic with your bucket allocation. If you know that travel is a priority in your life, make it a point to save for one big trip a year. Don’t accumulate the funds and let them sit for a trip 10 years down the road.

There are three ways in which you can fill this bucket:

- Jackpots – If you get a bonus or a windfall of some kind, use it to fuel your dream tank.

- Your Risk/Growth Bucket gets a positive hit and you score big. In this case, you may want to take some of your earnings and put one-third of these unexpected dividends into each bucket. You’re spreading out your risk, increasing your security and getting to achieve your dreams. Not bad!

- Save a set percentage of your income and hide it away until you’re able to purchase what you desire. This savings would be separate from what you’re using toward building your Money Machine.

Ultimately, asset allocation is just one step in creating the path to financial freedom. Armed with this division of savings, you can lay the foundation for enduring financial success in the future.

Saving is just the beginning of financial freedom

Attend the next Business Mastery event to get expert asset allocation strategies and more from the master himself, Tony Robbins.